#66.6: How Banks Create Money

Module 3 of 12: Loans Create Deposits, Not the Other Way Around

Forget what the textbook told you.

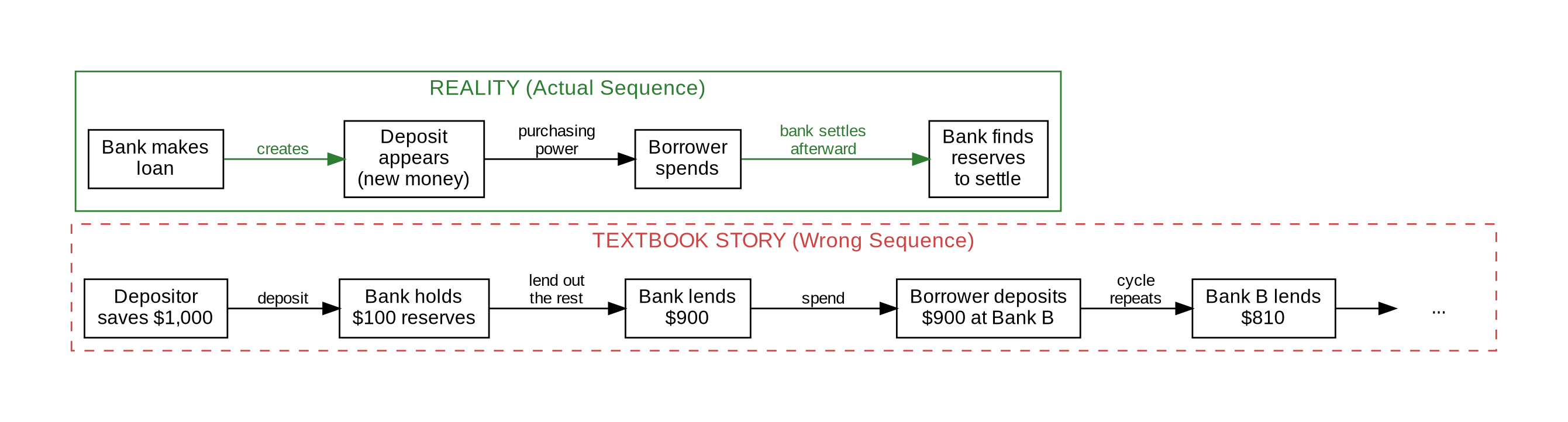

The standard story goes like this: you deposit $1,000 at a bank. The bank keeps 10% as reserves ($100) and lends out the remaining $900. The borrower spends that $900, and it ends up deposited at another bank. That second bank keeps $90 and lends $810. The chain continues, each step smaller, until the original $1,000 has multiplied into roughly $10,000 of total deposits across the banking system. This is the “money multiplier.” Neat. Tidy. Mechanical.

It is also wrong.

Not wrong in the sense that no multiplication occurs. Multiplication does occur. It is wrong about the sequence. It tells you deposits come first, then lending follows. The actual sequence runs the other way: lending comes first, and deposits appear as a consequence.

This distinction matters more than it sounds. If banks lend out existing deposits, they are intermediaries, middlemen passing money from savers to borrowers. If banks create deposits by lending, they are engines, generating new purchasing power that did not exist before the loan was signed. The first story implies a passive system constrained by how much people save. The second describes an active system constrained by willingness to lend, willingness to borrow, and the rules governing both.

Module 2 showed you what money is: mostly bank deposits, which are bank IOUs functioning as money through confidence. This module shows you how those deposits come into existence, what constrains the process, and why the constraints are looser than you expect.

Glossary

These terms appear throughout the module. Definitions here are specific to how they operate in the banking system, not their everyday meanings.

Balance sheet — A two-column ledger showing what an entity owns (assets) and what it owes (liabilities). The two sides must always be equal. Every bank loan changes both sides simultaneously.T-account — A simplified balance sheet drawn as a T-shape, with assets on the left and liabilities on the right. Used throughout this module to show how loans create deposits and how repayments destroy them.Assets — What you own or are owed. For a bank: loans it has made, bonds it holds, reserves at the central bank. For you: your deposit balance, your house, your savings.Liabilities — What you owe. For a bank: deposits it has promised to pay on demand, bonds it has issued, interbank borrowings. For you: your mortgage, your credit card balance.Equity (capital) — The difference between assets and liabilities. For a bank, equity is the shareholders’ money that absorbs losses before depositors take any hit. Basel III requires banks to hold minimum equity ratios.Deposits — Money held in your bank account. These are the bank’s liabilities (it owes you that money on demand) and your assets. Most of what we call “money” in the economy is deposits, created when banks make loans.Reserves — Money that banks hold in accounts at the central bank. Used to settle payments between banks. Think of reserves as the wholesale currency that banks use among themselves, distinct from the retail deposits that you and I use.Base money (monetary base) — Physical cash in circulation plus reserves held at the central bank. This is the money the central bank directly creates. A small fraction of total money in the economy.Broad money — The total money supply available for spending in the economy: cash plus all bank deposits. Roughly 97% of broad money is bank deposits. When this module says “money supply,” it means broad money.Policy rate — The interest rate set by the central bank that determines the cost of borrowing reserves overnight. In the US: the federal funds rate. In the UK: the Bank Rate. The central bank’s primary tool for influencing lending conditions.Interbank rate — The interest rate banks charge each other for overnight loans of reserves. Tracks close to the policy rate. When you hear “overnight rate” or “money market rate,” this is it.Standing facilities — Two permanent central bank services that bracket the interbank market. The lending facility lends reserves at a rate above the policy rate (ceiling). The deposit facility accepts reserves at a rate below the policy rate (floor).Risk-weighted assets — A bank’s assets adjusted for how risky regulators consider them. A government bond might carry a 0% risk weight (treated as riskless). A mortgage might carry 35%. A business loan might carry 100%. Capital requirements are measured against this adjusted total, not raw assets.Capital requirements (Basel III) — Rules requiring banks to hold minimum equity relative to risk-weighted assets. The key ratio is Common Equity Tier 1 (CET1): at least 4.5%, with buffers pushing the effective requirement to 7-13% depending on the bank’s systemic importance.Procyclical — Amplifying the direction the economy is already moving. A procyclical constraint loosens during booms (allowing more lending) and tightens during busts (forcing less lending). All four constraints on bank lending in this module are procyclical.Liquidity — The ability to meet payment obligations as they come due. A bank is liquid if it can settle deposits being withdrawn or transferred. Distinct from solvency.Solvency — Having assets worth more than liabilities. A bank is solvent if its loans and investments are worth enough to cover all its deposits and debts. A bank can be solvent but illiquid (assets are good but cannot be sold fast enough) or liquid but insolvent (can pay today but assets are underwater).Quantitative easing (QE) — Central bank purchases of financial assets (usually government bonds) paid for with newly created reserves. Expands the monetary base but does not directly create deposits in the real economy. Used when the policy rate has already hit zero.Collateral — An asset pledged as security for a loan. If the borrower defaults, the lender can seize the collateral. In a boom, rising asset prices make collateral look more valuable, supporting more lending. In a bust, falling prices shrink collateral values, triggering margin calls and forced sales.Originate-to-distribute — A banking model where the bank creates a loan, packages it into a security, sells the security to investors, and uses the freed-up capital to make more loans. The bank earns fees on origination volume rather than interest income on holdings. Separates the lending decision from the default risk.Securitization — The process of bundling many individual loans (mortgages, car loans, credit card debt) into a single tradeable security. The security pays investors from the cash flows of the underlying loans. Mortgage-backed securities (MBS) are the most common example.Endogenous — Generated from within the system. The money supply is endogenous because it is created by banks making loans, not injected from outside. Contrast with exogenous.Exogenous — Imposed from outside the system. The textbook model treats the money supply as exogenous, set by the central bank through reserves. This module shows that description is wrong.Write-off — When a bank accepts that a loan will not be repaid and removes it from the asset side of its balance sheet. The corresponding deposit has already been spent into the economy, so the write-off destroys bank equity (the loss falls on shareholders, not depositors, unless equity runs out).1 | The Textbook Version and Why It Persists

The money multiplier model appears in nearly every introductory economics textbook. Mankiw’s Principles of Economics presents it as the central mechanism of money creation (Mankiw, 2021). Samuelson and Nordhaus do the same (Samuelson & Nordhaus, 2009). Students learn a formula:

Money supply = Base money × (1 / Reserve ratio)If the reserve ratio is 10%, the multiplier is 10. Simple arithmetic. Exam-ready.

The model persists for three reasons. First, it produces a clean formula that can be tested on an exam. Second, it makes the central bank appear to be in control, since the central bank sets the reserve ratio and supplies base money. Third, it tells a comforting story: banks are constrained by deposits, so the system has a natural limit.

All three reasons serve pedagogy more than accuracy.

The Bank of England published a paper in 2014 titled “Money creation in the modern economy” that stated the issue plainly. The authors, Michael McLeay, Amar Radia, and Ryland Thomas, wrote that the money multiplier description reverses the actual sequence of events. In reality, banks do not wait for deposits before lending. Banks make lending decisions based on profitable opportunities and the price of reserves, then manage their reserve position afterward (McLeay, Radia & Thomas, 2014).

This is not a fringe position. The Bundesbank confirmed the same mechanism in its April 2017 Monthly Report: “In terms of the money creation process, the textbook depiction of the money multiplier fails to adequately capture the process” (Deutsche Bundesbank, 2017). The Federal Reserve Bank of New York published research reaching the same conclusion (Carpenter & Demiralp, 2010).

Three central banks, three confirmations. The textbook model is not how it works.

2 | How a Loan Actually Creates Money

Here is what happens when you walk into a bank and sign a loan agreement for $100,000.

The bank does not go to its vault, count out $100,000, and hand it to you. The bank does not check whether depositors have saved enough to cover your loan. The bank does not borrow $100,000 from another bank and pass it along.

The bank types two entries into its computer system.

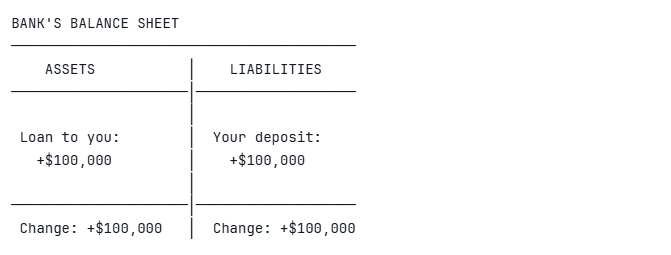

On your side:

• Your account balance increases by $100,000 (this is your asset, the bank’s liability)

• Your loan obligation increases by $100,000 (this is your liability, the bank’s asset)

On the bank’s balance sheet:

• Assets increase by $100,000 (the loan: your promise to repay)

• Liabilities increase by $100,000 (the deposit: the bank’s promise to pay you)

Both sides of the ledger grew by the same amount. The books balance. No money moved from anywhere else. $100,000 of new purchasing power now exists in the economy that did not exist five minutes earlier.

This is not a metaphor. It is double-entry accounting. The deposit is the loan, viewed from the other side of the balance sheet.

A T-Account Makes This Visible

Both sides grew by the same amount. Nothing was transferred. Nothing was intermediated. The bank created a matched pair: your promise to repay (bank’s asset) and the bank’s promise to pay you on demand (your deposit). The deposit is the money.

What Backs This New Money?

Your promise to repay. That is the bank’s asset. If you repay the loan on schedule with interest, the bank profits. If you default, the bank takes a loss. The new money is backed not by gold, not by government reserves, not by other people’s savings, but by a contract, a claim on your future income.

This connects directly to Module 1’s framework. The bank created a claim (the deposit/money) backed by another claim (the loan). Both claims rest on the assumption that the real economy will generate enough production for you to earn income, repay the loan, and keep the system running. The claim engine runs on expectations about the future.

3 | What Happens When the Borrower Spends

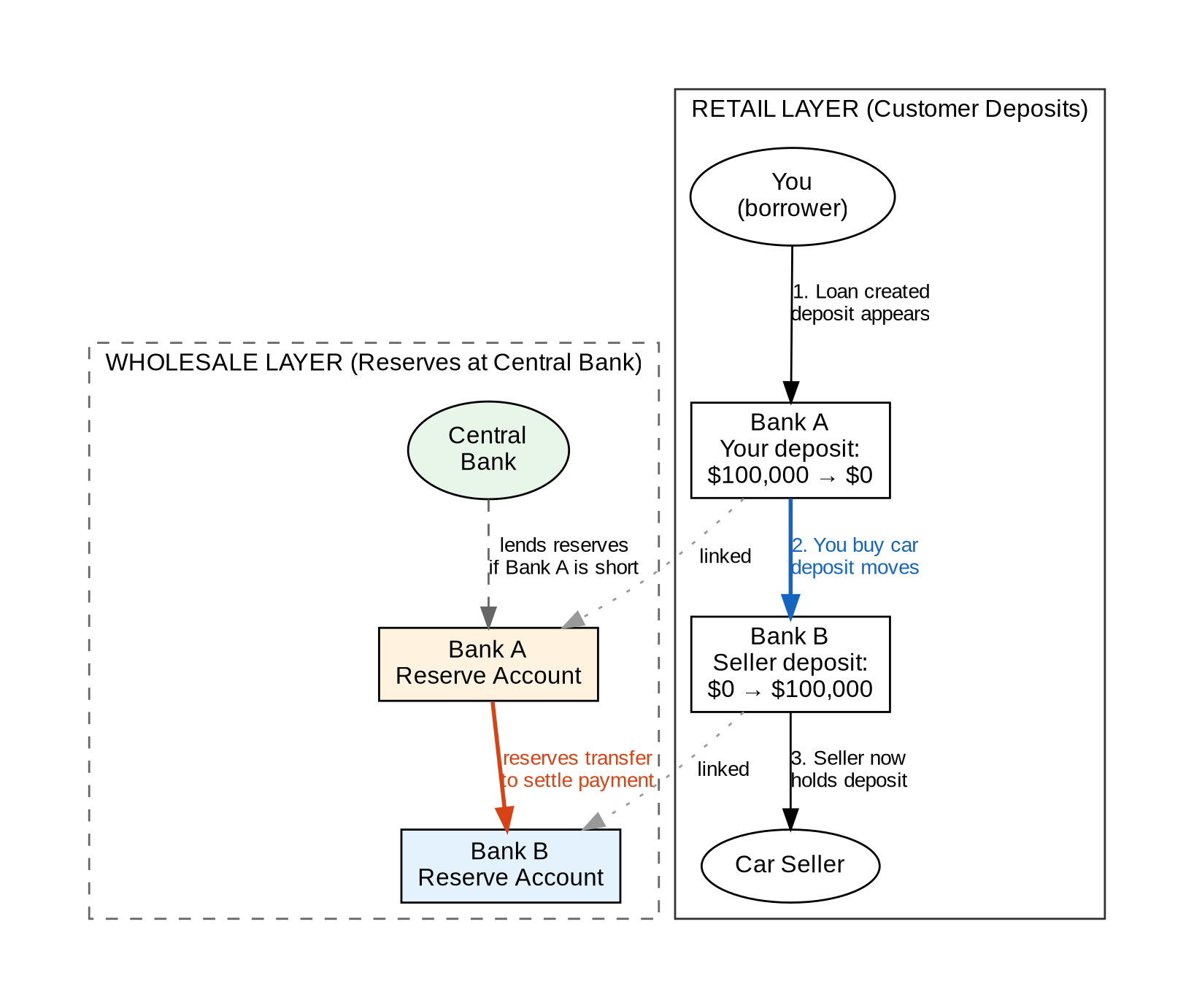

The moment you spend that $100,000, the deposit moves. Say you buy a car. The money transfers from your account at Bank A to the car dealer’s account at Bank B.

Now something shifts at the wholesale level. Bank A lost a deposit. Bank B gained one. But Bank A still has the loan asset. Its balance sheet is now lopsided: more assets than liabilities. Bank B has the opposite problem: a new deposit liability with no corresponding loan asset.

This is where reserves come in.

Bank A needs to transfer reserves to Bank B to settle the payment. Reserves are the money that banks use between themselves, held in accounts at the central bank. Think of reserves as the wholesale layer underneath the retail deposit layer. When you move a deposit from one bank to another, reserves move in the same direction to settle the transaction.

If Bank A has enough reserves, the settlement happens smoothly. If Bank A runs short, it borrows reserves overnight from another bank that has excess, or directly from the central bank. The price of borrowing reserves overnight is the interbank rate, which tracks closely to the central bank’s policy rate.

This is the key inversion from the textbook story. The textbook says: reserves first, then lending. Reality says: lending first, then the bank acquires reserves to settle. Banks do not check their reserve balance before making a loan. They make the loan, create the deposit, and then manage their reserve position through interbank markets and central bank facilities.

4 | What Constrains Banks If Not Reserves?

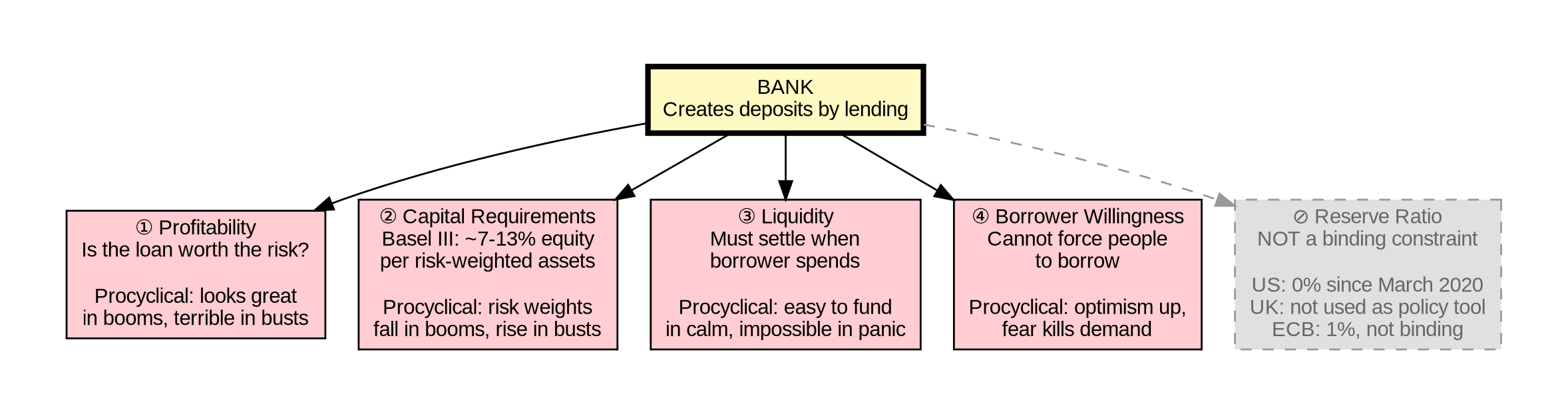

If banks can create deposits by lending, why don’t they lend without limit? Four constraints operate, and none of them is the textbook reserve ratio.

Constraint 1: Profitability

Banks lend to make money. The spread between the interest rate they charge on loans and the interest rate they pay on deposits (or reserves) determines profit. If lending opportunities look risky or unprofitable, banks lend less. No regulation required. Banks self-limit when the expected return does not justify the risk.

This constraint is procyclical. In a boom, everything looks profitable. Asset prices rise, collateral values increase, borrowers appear creditworthy. Banks lend more. In a bust, risk appears everywhere. Banks lend less, call in loans, tighten standards. The constraint amplifies both directions instead of dampening them.

Constraint 2: Capital Requirements

This is the binding regulatory constraint. Capital requirements, set by the Basel framework (currently Basel III), require banks to hold a minimum ratio of equity capital relative to their risk-weighted assets. Under Basel III, the minimum Common Equity Tier 1 (CET1) ratio is 4.5% of risk-weighted assets, with additional buffers that bring the effective requirement to roughly 7-13% depending on the bank’s size and systemic importance (Basel Committee on Banking Supervision, 2011).

In plain terms: for every $100 of (risk-weighted) loans a bank creates, it must have roughly $7-$13 of shareholders’ equity absorbing potential losses. If a bank’s capital falls below the requirement, regulators restrict further lending and may force the bank to raise new equity or shrink its balance sheet.

Capital requirements are a real constraint. They cap the total volume of lending relative to the bank’s equity cushion. But they also have a procyclical problem. In a boom, rising asset prices reduce apparent risk weights, making the same capital support more lending. In a bust, falling prices increase risk weights, forcing deleveraging at the worst moment.

Constraint 3: Liquidity Management

When a bank makes a loan and the borrower spends the deposit, reserves leave the bank. The bank must be able to settle payments. If a bank lends aggressively and many borrowers spend quickly, the bank faces a reserve drain. It must fund that drain through interbank borrowing, central bank facilities, or by attracting new deposits from other banks’ customers.

The cost of this funding matters. If interbank rates rise (because the central bank is tightening policy), the cost of managing reserves after lending increases. This makes some loans unprofitable, reducing lending at the margin.

Liquidity regulations (the Liquidity Coverage Ratio and Net Stable Funding Ratio under Basel III) formalize this by requiring banks to hold enough high-quality liquid assets to survive 30 days of stressed outflows (Basel Committee on Banking Supervision, 2013).

Constraint 4: Borrower Willingness

Banks cannot force people to borrow. In a recession, even if banks are willing to lend at low rates, households and firms may not want to take on debt. Their incomes are uncertain, their assets are losing value, and the future looks risky. This is what economists call “pushing on a string,” the central bank floods the system with cheap reserves, banks are technically able to lend, but nobody wants to borrow.

Japan from the 1990s onward demonstrated this constraint vividly. The Bank of Japan reduced interest rates to zero, then introduced quantitative easing, flooding the banking system with reserves. Bank lending barely responded for over a decade. The constraint was not reserve supply. It was demand for credit in a deflating economy (Koo, 2009).

The Missing Constraint: Reserves

Notice what is not on this list. The reserve requirement is not a binding constraint on modern bank lending. Most developed economies have either reduced reserve requirements to minimal levels or eliminated them entirely. The Federal Reserve set reserve requirements to zero in March 2020 (Board of Governors of the Federal Reserve System, 2020). The Bank of England has not used reserve requirements as a monetary policy tool for decades. The European Central Bank maintains a 1% ratio, which is not binding for most banks.

The textbook gives reserves center stage. In practice, they are a plumbing detail, not a control lever.

5 | The Central Bank’s Actual Role

If the central bank does not control money creation through reserve requirements, what does it do?

It sets the price of reserves, not the quantity.

The central bank’s primary tool is the policy rate: the interest rate at which banks can borrow reserves overnight. In the US, this is the federal funds rate. In the UK, the Bank Rate. In the eurozone, the main refinancing rate.

When the central bank raises the policy rate, borrowing reserves becomes more expensive. Banks pass this cost to borrowers through higher loan rates. Higher loan rates reduce the demand for borrowing and make some lending opportunities unprofitable. Money creation slows.

When the central bank cuts the policy rate, reserves become cheaper. Banks can lend at lower rates. Lower rates stimulate borrowing demand and make previously marginal projects profitable. Money creation speeds up.

The mechanism is indirect. The central bank does not tell banks how much to lend. It adjusts the cost of the raw material (reserves) and lets the banking system respond. This is price-based control rather than quantity-based control.

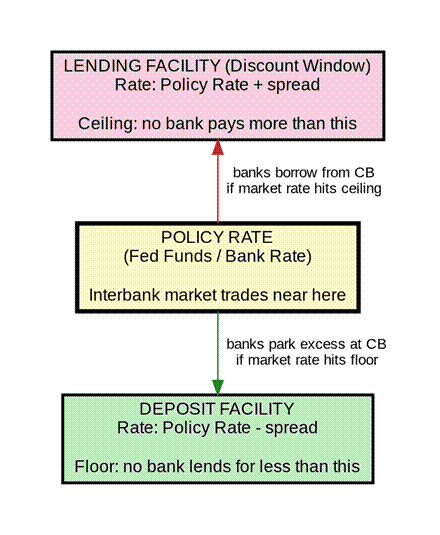

Standing Facilities

Central banks also provide two standing facilities that set a corridor around the policy rate.

The lending facility (called the discount window in the US) allows banks to borrow reserves from the central bank at a rate slightly above the policy rate. This provides a ceiling: no bank needs to pay more than the lending facility rate for reserves, because it can always borrow from the central bank.

The deposit facility allows banks to park excess reserves at the central bank and earn interest at a rate slightly below the policy rate. This provides a floor: no bank will lend reserves to another bank for less than it can earn by parking them at the central bank.

The policy rate sits between these two bounds. The interbank market for reserves operates within this corridor.

Lender of Last Resort

In a crisis, the central bank’s role shifts from routine price-setting to emergency provision. When banks cannot borrow reserves from each other (because nobody trusts anybody’s balance sheet), the central bank steps in as lender of last resort. It provides reserves to banks that have adequate collateral but face temporary liquidity problems.

This connects back to Module 0’s distinction between liquidity and solvency. The central bank can solve liquidity crises by providing reserves. It cannot solve solvency crises. If a bank’s assets are genuinely worth less than its liabilities, no amount of reserve lending fixes the problem. The central bank’s dilemma in a crisis is that it often cannot tell the difference in real time.

Walter Bagehot articulated the classical rule in 1873: lend freely, at a high rate, on good collateral (Bagehot, 1873). The rule sounds simple. Applying it when markets are panicking and collateral values are uncertain is not.

6 | Quantitative Easing: When the Price Tool Stops Working

Sometimes the policy rate hits zero and the economy still contracts. Borrowers do not want to borrow even at near-zero rates. Banks do not want to lend because everything looks risky. The price tool has reached its floor.

Central banks respond with quantitative easing (QE): they buy financial assets (usually government bonds) from banks and other financial institutions, paying with newly created reserves. The central bank’s balance sheet expands on both sides: assets grow (the bonds it bought) and liabilities grow (the reserves it created to pay for them).

QE does not directly create deposits in the real economy. It creates reserves in the banking system. The hope is that by removing safe assets (government bonds) from the market, investors will be pushed toward riskier assets (corporate bonds, equities, property), driving up prices, loosening financial conditions, and encouraging spending and investment.

Whether QE works as intended is disputed. The Bank of England estimated that its first round of QE (2009-2012) raised GDP by 1.5-2% (Joyce et al., 2012). Critics argue QE primarily inflated asset prices, benefiting asset holders disproportionately while doing little for wage earners and borrowers in the real economy (Haldane, 2014).

For this course, the mechanism matters more than the debate about effectiveness. QE shows what happens when the central bank exhausts its normal tool (the policy rate) and resorts to directly expanding the base money supply. Yet even this does not control the broad money supply. Reserves can pile up in the banking system without generating new lending if the other constraints (profitability, capital, borrower willingness) remain binding.

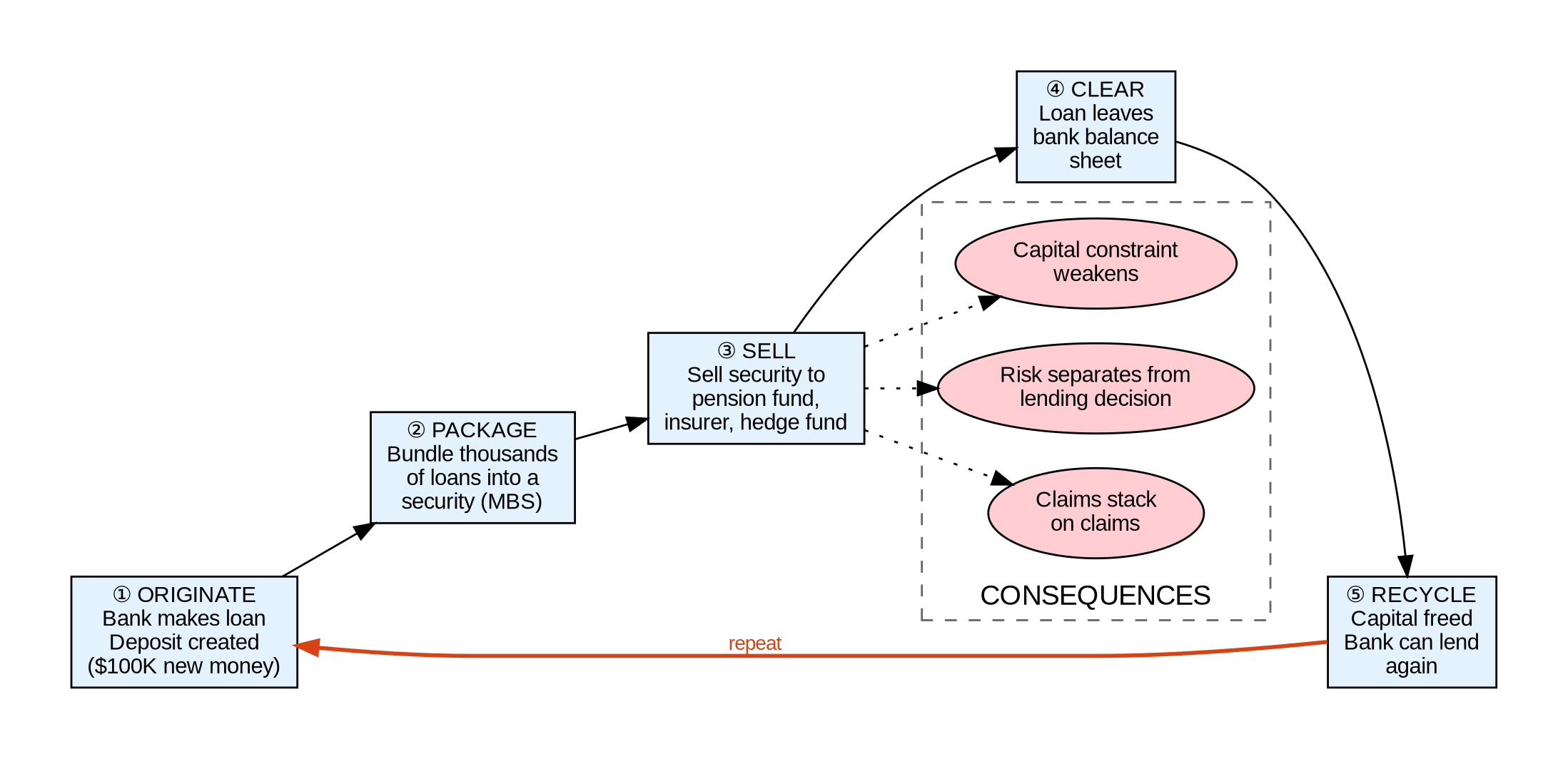

7 | The Escape Hatch: Selling the Loan

The four constraints in Section 4 assume the bank holds the loan on its balance sheet for the life of the contract. That assumption held for most of banking history. It stopped holding in the 1970s and 1980s when banks discovered they could sell loans.

Walk through the sequence:

1. Bank creates a $100,000 mortgage. Deposit appears. Balance sheet grows on both sides.

2. Bank packages the mortgage (often with thousands of others) into a security, a bond backed by the mortgage payments.

3. Bank sells the security to a pension fund, insurance company, hedge fund, or another bank.

4. Bank receives cash or reserves for the sale. The loan leaves its balance sheet.

5. The bank’s capital ratio improves because the risk-weighted asset is gone.

6. The bank can now create another loan.

Repeat.

This model is called originate-to-distribute. The bank stops being a warehouse that holds loans and becomes a pipeline that manufactures them, packages them, sells them, and recycles the capacity.

Three consequences follow, and all of them matter for later modules.

First: capital constraints weaken. If the bank sells the loan, its balance sheet does not grow, so it does not need more capital to keep lending. Constraint 2 from Section 4 loosens dramatically. The binding question shifts from “how much capital do I have” to “can I find a buyer for this loan.”Second: risk separates from decision-making. The bank that decides whether to approve the loan is no longer the institution bearing the loss if the borrower defaults. The buyer of the security bears that risk. But the buyer is distant from the borrower. The buyer relies on credit ratings, packaging quality, and statistical models rather than direct knowledge of whether the borrower can repay. The person deciding to lend and the person absorbing the default risk are now different people in different institutions in different countries. Incentives split.Third: claims stack on claims. The mortgage-backed security is a claim on the mortgage payments. But that security can itself be used as collateral for short-term borrowing (this is Module 7’s repo market). And the short-term borrowing can fund the purchase of more securities. Each layer sits one step further from the original borrower and the original deposit that was created when the loan was made.The 2008 financial crisis ran on this mechanism at full speed. US banks originated mortgages, packaged them into mortgage-backed securities (MBS), sold the MBS to investors worldwide, freed up capital, originated more mortgages, repeated. Between 2003 and 2007, US mortgage origination totaled roughly $3.6 trillion per year, with the majority securitized and sold (Inside Mortgage Finance, 2008). When borrowers defaulted, losses did not sit with the originating banks. They sat with whoever held the securities. But nobody knew exactly who held what, because the securities had been sliced, repackaged, and resold multiple times. Trust collapsed across the entire wholesale funding market simultaneously.

The originate-to-distribute model does not break the four constraints from Section 4. It routes around them. Capital requirements still exist, but selling the loan clears the capital charge. Liquidity management still matters, but the sale brings in reserves. Profitability improves because the bank earns origination fees on volume rather than interest income on holdings. Only borrower willingness remains fully intact.

This is a preview. Module 7 (repo and haircuts) and Module 8 (shadow banking) will map the full plumbing of how these sold claims circulate, get used as collateral, and seize up when confidence breaks. For now, hold the core point: the constraints that appear to limit money creation have a back door, and the banking system found it.

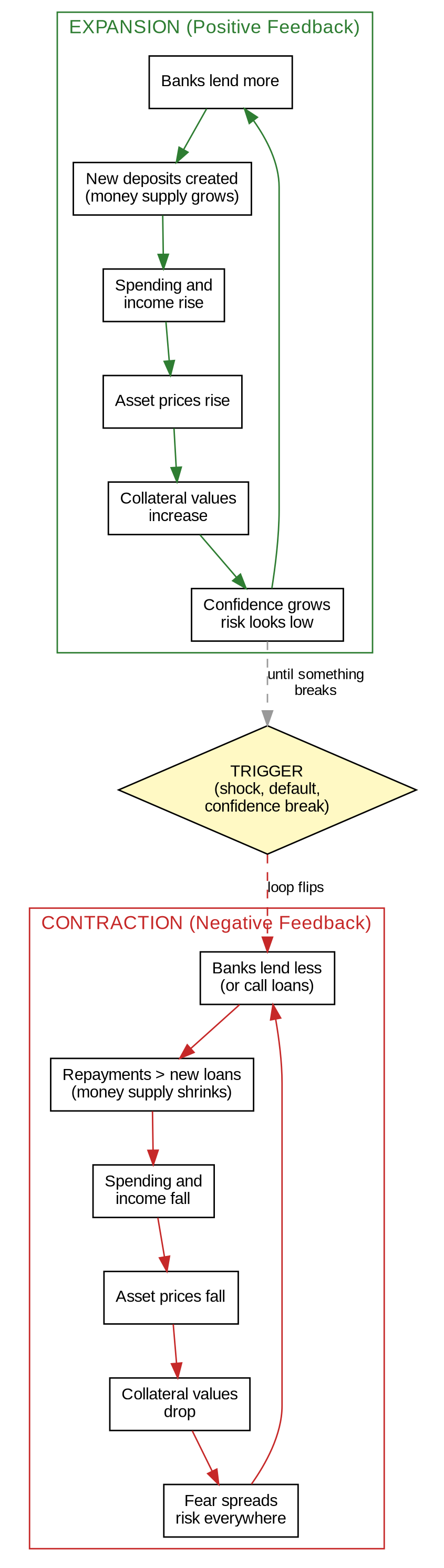

8 | Why This Makes the System Inherently Procyclical

Gather the pieces

Banks create money by lending. They lend more when the economy looks good. Their lending creates deposits, which become spending, which becomes income for someone else, which makes the economy look better. More lending follows. This is a positive feedback loop with no internal dampener.

Capital requirements offer some restraint but are themselves procyclical. In the boom, risk appears low, risk weights fall, capital supports more lending. In the bust, risk materializes, risk weights rise, capital forces contraction.

The central bank’s interest rate influences the cost of reserves but does not cap the volume of lending. The rate tool operates with a lag (changes take 12-18 months to filter fully through the economy) and cannot address localized credit bubbles without affecting the entire economy.

Borrower willingness swings with sentiment. In the boom, optimism drives borrowing. In the bust, fear halts it.

Every constraint is procyclical. Every constraint amplifies the direction the system is already heading. And as Section 7 showed, the constraints themselves have a back door: banks can sell their loans, clear the capital charge, and restart the pipeline.

Module 2 introduced the circular dependency: variable money supply and variable asset values feeding each other with no anchor. This module shows why that circular dependency exists. The money creation mechanism accelerates in both directions. It is not a bug. It is the architecture.

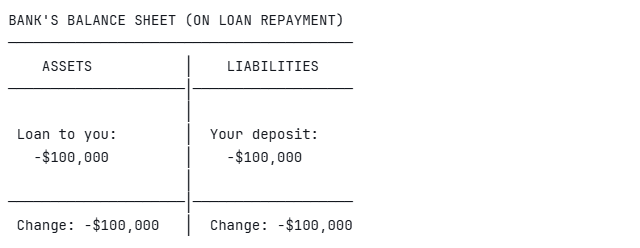

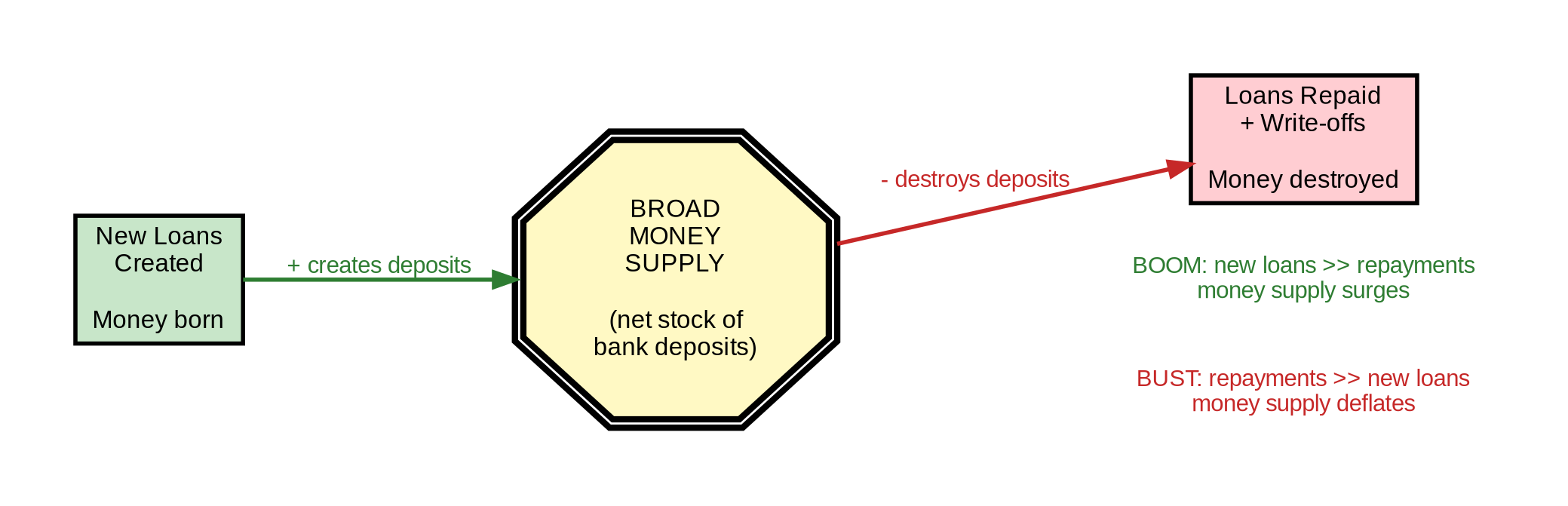

9 | Loan Repayment Destroys Money

The process runs in reverse.

When you repay a loan, your deposit shrinks (your asset declines) and your loan balance shrinks (the bank’s asset declines). Both sides of the bank’s balance sheet contract. The money that was created when the loan was made is destroyed when the loan is repaid.

The deposit vanishes. The purchasing power ceases to exist. Nobody else receives it. It is not transferred, not recycled, not saved. It is extinguished.

This means the broad money supply in an economy is the net result of two flows:

New loans created minus existing loans repaid = change in money supply

If banks create more loans than are being repaid, the money supply expands. If repayments exceed new lending, the money supply contracts. The money supply is a stock determined by two opposing flows.

In a credit boom, new lending far exceeds repayments. Money supply surges. In a credit crunch, repayments exceed new lending (or banks write off bad loans, which also destroys the corresponding deposit claim). Money supply shrinks.

This is why recessions associated with credit contractions are so severe. The money supply itself is deflating. There is less money to buy goods, pay wages, service debts. The entire economy is trying to transact with a shrinking medium.

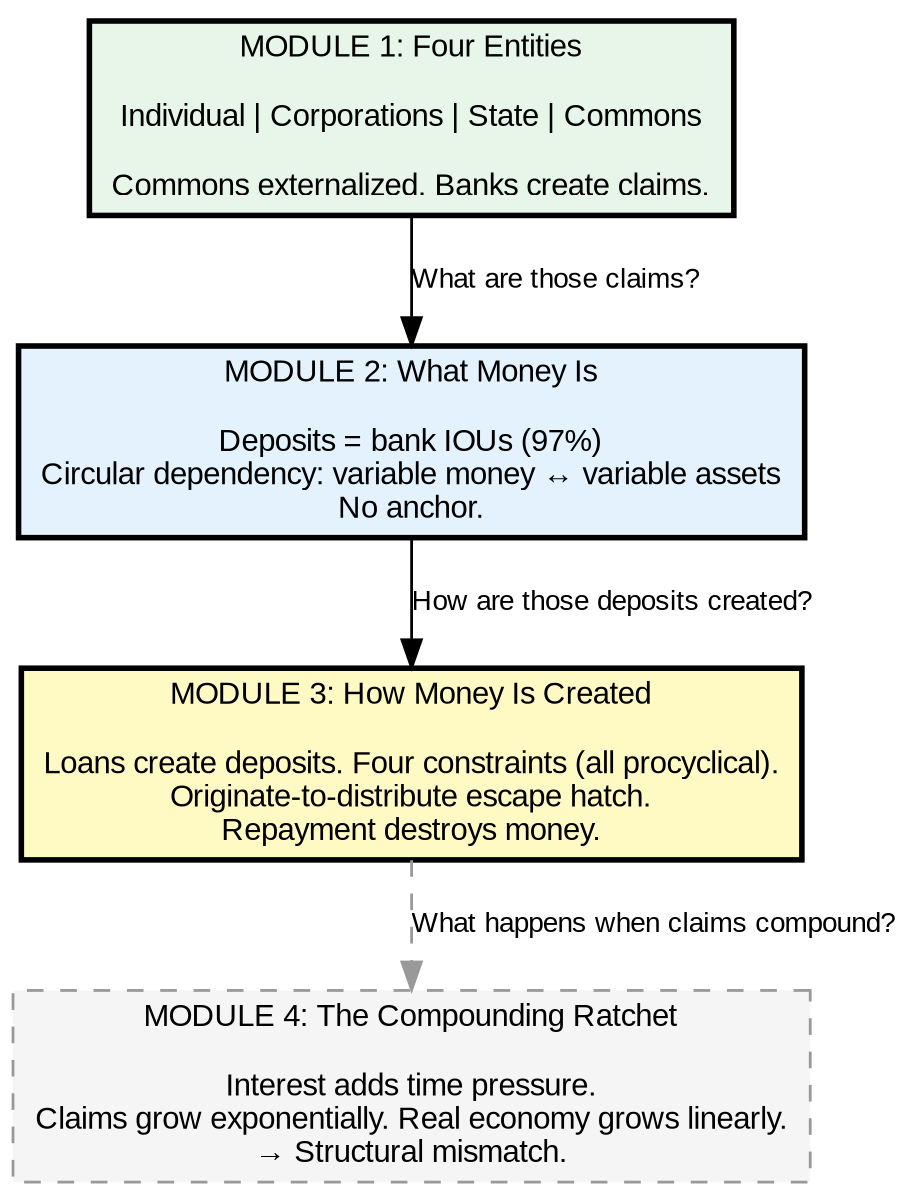

10 | The Connection to Modules 1 and 2

Module 1 established four irreducible entities: Individual, Collective Production, Governance, and Commons. It showed that modern finance externalizes Commons and concentrates claim production in the banking system.Module 2 showed that money is mostly bank deposits, bank IOUs that function as money through confidence. It introduced the circular dependency: variable money and variable asset values feeding each other with no anchor.Module 3 reveals the engine behind both. Banks create money by lending. The money supply is not a fixed stock managed by the government. It is a dynamic variable driven by millions of individual lending and repayment decisions, influenced by the central bank’s interest rate but not controlled by it.The claim engine from Module 1 is this mechanism. Banks produce claims (deposits) backed by other claims (loans) backed by expectations about real production. When expectations align with reality, the system generates productive credit. When expectations detach, when claims compound faster than production can support them, the system generates bubbles, crises, and crashes.

The circular dependency from Module 2 is powered by this engine. Banks create deposits to fund asset purchases. Asset prices rise. Rising prices make collateral more valuable. More valuable collateral enables more lending. More lending creates more deposits. The loop has no natural stopping point because both money and asset values are endogenous: both are products of the same system rather than external anchors.

And the real constraints, the ones that bind in practice, are all procyclical. The system accelerates in the direction it is already moving, upward or downward, with no internal mechanism to prevent overshooting.

11 | What You Now Know That Most People Do Not

Most people believe banks lend out deposits. You now know banks create deposits by lending. The sequence runs: lending first, deposits second. This makes banks money creators, not intermediaries.

Most people believe the central bank controls the money supply through reserve requirements. You now know the central bank sets the price of reserves, not the quantity of money. The money supply is determined by bank lending decisions, borrower willingness, and regulatory constraints, none of which the central bank directly controls.

Most people believe there is a stable “money multiplier” linking base money to broad money. You now know this ratio is not stable and the causal direction is inverted. Banks do not multiply reserves into deposits. Banks create deposits and then acquire reserves to settle.

Most people believe loan repayment “recycles” money back to the bank. You now know loan repayment destroys money. The deposit vanishes. This means the money supply can shrink, and does shrink, whenever loan repayments exceed new lending.

Most people believe QE “prints money.” You now know QE creates reserves, the wholesale layer, not deposits, the retail layer. Whether QE translates into real economy spending depends on whether the reserves trigger new bank lending, which depends on the four constraints already discussed.

Most people believe banks hold the loans they make. You now know banks can sell loans, clearing their balance sheets and recycling their capacity to lend again. This originate-to-distribute model routes around capital and liquidity constraints, separates the lending decision from the default risk, and creates layers of claims on claims that connect Modules 7, 8, and 10.

Hold all of this. Module 4 picks up where the system meets time: interest rates, compounding, and what happens when claims accumulate faster than the real economy can service them.

Exercises

Simple Drill (10 minutes)

Walk through one $100,000 mortgage step by step on a T-account.

Step 1: Draw the bank’s balance sheet before the loan (some existing assets and liabilities).

Step 2: Show what changes when the loan is made (new asset: loan; new liability: deposit).

Step 3: The borrower buys a house. The deposit transfers to the seller’s bank. Show the reserve movement.

Step 4: Over 10 years, the borrower repays the loan. Show the balance sheet shrinking as each repayment destroys money.

At the end, answer: how much money was created? How much was destroyed? What was the net effect on the economy’s money supply?

Check Questions

A bank has $10 billion in deposits and $500 million in reserves. It makes a $50 million loan. Where do the funds come from?

Answer: Nowhere external. The bank creates a $50 million deposit (new liability) matched by a $50 million loan (new asset). No reserves are needed at the moment of creation. Reserves are needed later, when the borrower spends and the deposit moves to another bank.

If every borrower in the economy repaid all outstanding loans simultaneously, what would happen to the money supply?

Answer: It would collapse to near zero. Almost all broad money is bank deposits created through lending. If all loans were repaid, all corresponding deposits would be destroyed. Only base money (physical cash and central bank reserves) would remain. The economy would have almost no medium of exchange.

Visual Exercise

Draw a timeline showing one credit cycle:

Phase 1 (Expansion): New loans exceed repayments. Money supply grows. Asset prices rise. Collateral values increase. Banks lend more. Label the positive feedback loop.

Phase 2 (Peak): Lending slows. Some borrowers struggle. Default rates tick up. Banks tighten standards.

Phase 3 (Contraction): Repayments and write-offs exceed new loans. Money supply shrinks. Asset prices fall. Collateral values drop. Banks lend less. Label the negative feedback loop.

Phase 4 (Intervention): Central bank cuts rates, provides emergency reserves. Government guarantees deposits. Fiscal spending adds non-bank money to the economy.

Mark where each of the four constraints (profitability, capital, liquidity, borrower willingness) becomes binding in each phase. Which constraint dominates during expansion? During contraction?

References

Bagehot, W. (1873). Lombard Street: A Description of the Money Market. London: Henry S. King & Co.

Basel Committee on Banking Supervision (2011). “Basel III: A global regulatory framework for more resilient banks and banking systems.” Bank for International Settlements. link

Basel Committee on Banking Supervision (2013). “Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools.” Bank for International Settlements. link

Board of Governors of the Federal Reserve System (2020). “Federal Reserve Actions to Support the Flow of Credit to Households and Businesses.” March 15, 2020. link

Carpenter, S. & Demiralp, S. (2010). “Money, Reserves, and the Transmission of Monetary Policy: Does the Money Multiplier Exist?” Federal Reserve Board FEDS, 2010-41. link

Deutsche Bundesbank (2017). “The role of banks, non-banks and the central bank in the money creation process.” Monthly Report, April 2017. link

Haldane, A. (2014). “Unfair Shares.” Speech at Bristol Festival of Ideas, May 2014. Bank of England. link

Inside Mortgage Finance (2008). The 2008 Mortgage Market Statistical Annual. Bethesda, MD: Inside Mortgage Finance Publications.

Joyce, M., Tong, M. & Woods, R. (2012). “The United Kingdom’s quantitative easing policy: design, operation and impact.” Bank of England Quarterly Bulletin, Q3 2012.

Koo, R. (2009). The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession. Singapore: John Wiley & Sons.

Mankiw, N.G. (2021). Principles of Economics. 9th ed. Boston: Cengage Learning.

McLeay, M., Radia, A. & Thomas, R. (2014). “Money creation in the modern economy.” Bank of England Quarterly Bulletin, Q1 2014. link

Samuelson, P. & Nordhaus, W. (2009). Economics. 19th ed. New York: McGraw-Hill.

What Comes Next

Module 3 mapped the engine: banks create money through lending, and the process is constrained by profitability, capital, liquidity, and borrower willingness, all of which amplify the cycle rather than dampen it. You also saw the escape hatch: banks can sell their loans, clear the constraints, and restart the pipeline, which is how the system scales beyond what any single bank’s balance sheet could support. You now know the money supply is endogenous, created by the banking system through credit decisions, not exogenous, set by the central bank through reserve management.

Module 4 introduces time into the machine. Interest and compounding take the money creation mechanism and add a ratchet: each dollar of debt demands more dollars in the future. When claims compound faster than the real economy grows, the system builds pressure. Module 4 traces how interest rates distribute this pressure, who absorbs it, and why the mathematics of compounding on a finite planet creates structural contradictions that no amount of central bank management can resolve.

The engine is running. Next, we watch it accelerate.